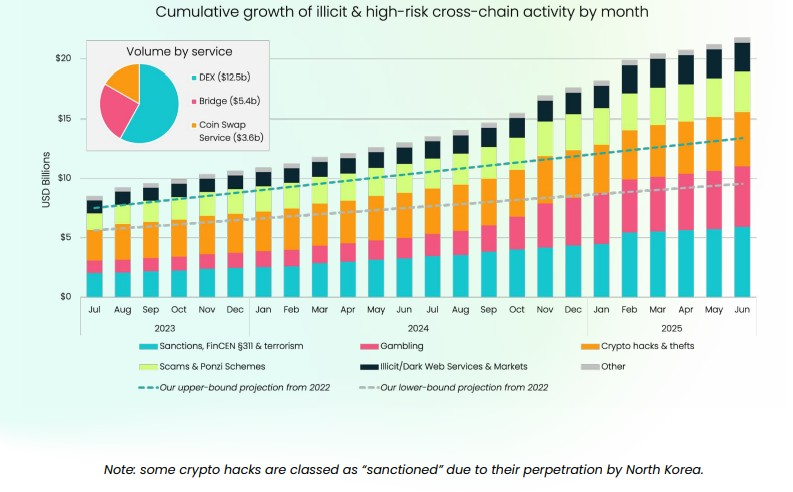

A staggering $21.8 billion in illicit and high-risk cryptocurrency transactions have moved through cross-chain bridges.

Also they have used decentralized exchanges (DEXs) and coin swap services over the past two years, according to a new report by UK-based blockchain analytics firm Elliptic.

The figure represents a dramatic 211% surge from $7 billion in 2023, signaling a seismic shift in how criminals operate in the decentralized finance (DeFi) space.

What was once a niche practice among advanced traders has become a sophisticated laundering mechanism for cybercriminals, with 12% of these transactions reportedly linked to North Korean actors.

As the blockchain ecosystem has expanded beyond just Bitcoin and Ethereum into a multichain environment, so too have the methods used to obscure the source of illicit funds.

Criminals Exploit Blockchain Bridges and Multi-Hop Tactics to Obscure Trails

Elliptic’s 2025 Crosschain Crime Report describes how cybercriminals are using “structured” and “multi-hop” laundering techniques to bypass blockchain transparency.

Structured chain-hopping involves splitting stolen or illicit crypto and sending it across several blockchains simultaneously.

On the other hand, multi-hop techniques involve sequential transfers from chain to chain, both designed to confuse forensic analysts and inflate transaction costs to dissuade tracking. These laundering methods are now routine in high-value hacks.

For example, North Korea-linked hackers allegedly used these tactics to launder $75 million stolen from an exchange, routing the funds through Bitcoin, Ethereum, Arbitrum, Base, and Tron.

These activities underscore how bridges have evolved into key infrastructure for cross-chain financial obfuscation.

Also Read: Crypto Investigators Warn Crypto Users of Fake Aave Site Topping Google Search, Details Inside

Chain Hopping No Longer Exclusive to State-Sponsored Attacks

The use of cross-chain laundering has become so widespread that it now includes smaller-scale fraud and individual criminals, not just nation-state actors or massive exploiters.

In one recent case, a UK fraudster involved in a $200,000 scam used chain hopping to split funds across 90 different assets across multiple blockchains, eventually spending the proceeds on online gambling.

According to Elliptic’s lead crypto threat researcher Arda Akartuna, nearly one-third of blockchain investigations now require tracing funds through three or more chains.

The trend highlights the mainstream adoption of advanced laundering methods and the growing challenges law enforcement faces when tracking illicit crypto flows.

Decentralized Exchanges and Aggregators are Key Entry Points in Laundering Schemes

Decentralized exchanges, once celebrated for their transparency and openness, are now playing an increasingly pivotal role in crypto laundering.

Criminals use DEXs to swap low-liquidity tokens into stablecoins or more widely accepted assets like Ether, often bypassing centralized exchanges that enforce Know Your Customer (KYC) policies.

A case study in Elliptic’s report details how hackers exploited Cetus, a liquidity provider on the Sui blockchain, to steal over $200 million.

The attackers used a DEX to convert USDT into USDC before bridging to Ethereum, where a DEX aggregator converted the stablecoins into Ether.

By doing so, they avoided centralized controls, exploiting the permissionless nature of DEXs and the inability to freeze native assets like ETH.

Sophisticated laundering tactics also include routing funds through obscure token pairs and using smart contracts to disguise transactions further.

Also Read: Crypto Investigator Warns Against Fake HyperLend Ads On Google That Could Lead to Phishing Scams

Broader Industry Scams Amplify Concerns About Crypto Fraud Ecosystem

The alarming growth in cross-chain laundering is part of a wider pattern of fraud and deception in the crypto space.

Authorities in Vietnam recently dismantled a $400 million pyramid scheme known as Matrix Chain, which promised huge profits through a multi-level marketing model.

In another case, cybercriminals exploited fake Google ads to impersonate Four.Meme on the BNB Chain, stealing wallet credentials from unsuspecting users.

Meanwhile, Self Chain, a prominent blockchain project, has come under fire after its CEO was terminated over allegations of involvement in a $50 million over-the-counter (OTC) Ponzi scheme.

These incidents further highlight the pressing need for stronger regulatory oversight, more robust AML protocols.

Also there is better investor education as the crypto ecosystem becomes increasingly complex and vulnerable to abuse.

{kind=link}